Last week, while booking a flight to Pune for a client meeting, something caught my eye.

Every single payment offer on the travel portal was pushing one thing — EMIs. Whether it was a credit card or a buy-now-pay-later option, the message was clear: break it up into monthly payments, and you get a discount. Pay in full? No reward, no incentive.

And this trend reflects across different segments, we’re being nudged to borrow for everything.

We are embracing the credit lifestyle with open arms.. Phones, luxury cars and even holidays are being financed into easy EMI payments. This is an obsession that runs deep and has severe ramifications, some of which have already begun to unfold- rising delinquencies in microfinance, coercive recovery tactics by lenders, and a growing habit of borrowing without budgeting. The question is, are we noticing these dangerous signs before it’s too late?

In this edition, we’ll unpack:

1. Credit everywhere – the anatomy of India’s EMI culture

2. The maths no one does – How small EMIs hide big traps

3. Why we fall for it – status symbolism, psychology, and money habits

4. International context: Learning from global credit cycles

Let’s go!

Credit everywhere – the anatomy of India’s EMI culture

Credit, when channelled productively, drives growth. It powers entrepreneurship, supports infrastructure, and drives long-term capital formation.

But credit for consumption is a whole different ballgame. It doesn’t create productive capacity. It simply brings future spending into the present, often for things that depreciate quickly or offer no long-term value. Over time, it can quietly distort our sense of affordability, making monthly outflows feel manageable even as overall debt piles up.

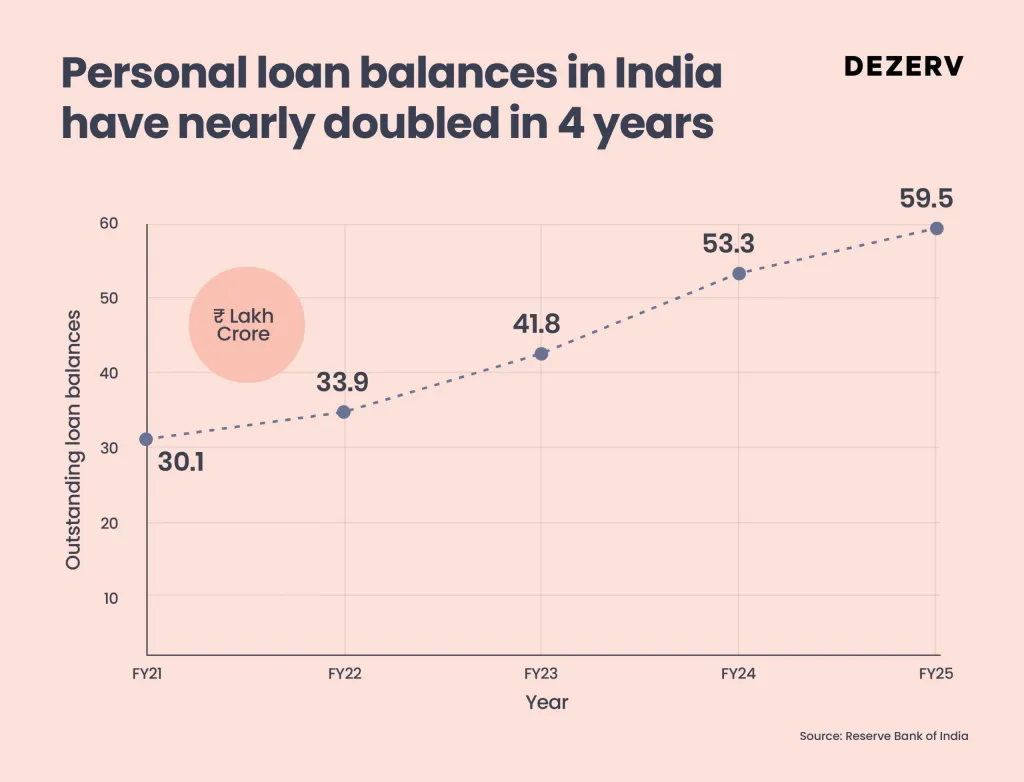

Personal loan balances in India have nearly doubled in four years, rising from ₹30.1 lakh crore in March 2021 to ₹59.5 lakh crore by March 2025 — a compound annual growth rate of 18.2%, far outpacing wage growth. With personal loans growing at a breakneck speed, the central bank stepped in late last year and came out with a circular, instructing banks and Non-Banking Financial Companies (NBFCs) to hold more capital against unsecured loans and apply stricter checks on lending.

Crucially, this number doesn’t include the mushrooming informal ecosystem of digital loan apps and shadow lenders, which have quietly expanded across Tier-2 and Tier-3 India. What looks like a formal credit boom is only the visible part of a much larger behavioural shift — one that’s normalising debt as a default setting for consumption.

And nowhere is this shift more visible than in our day-to-day purchases. Industry estimates suggest that roughly 40% of smartphones sold in India are purchased through EMIs — a number that climbs to over 70% when it comes to iPhones.

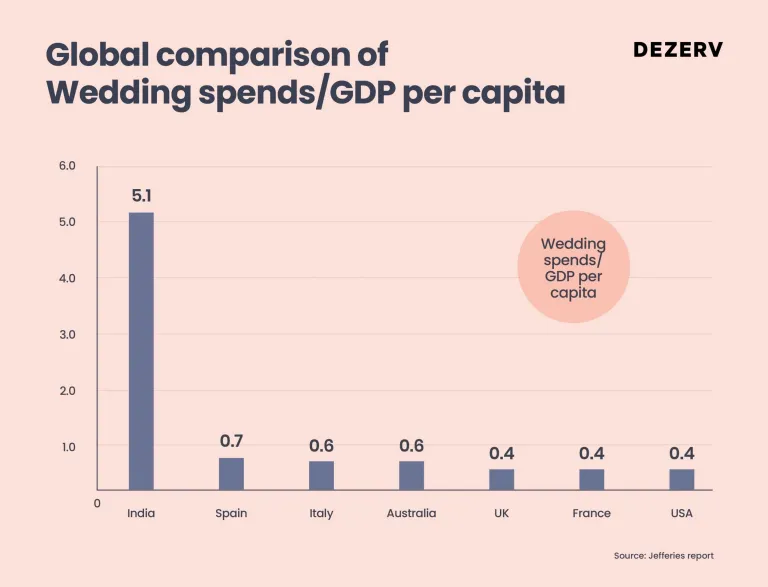

Not far behind are weddings. A Jefferies report pegs the Indian wedding industry at a staggering $130 billion, second only to groceries in terms of household spending. The average Indian wedding now costs ₹12 lakh- in some cases, more than what families spend on 18 years of a child’s education.

This chart shows just how disproportionately India spends on weddings.

While the average wedding spend in India is around $15,000, it amounts to 5.1 times the country’s per capita GDP — far higher than any other country on the list. In contrast, countries like the US, UK, and France spend more in absolute terms (up to $35,000), but relative to income, it’s only 0.4 times their GDP per capita.

A large chunk of this spend is financed through credit. Personal loans, gold loans, even buy now pay later (BNPL) schemes are being used to fund what should be a celebration, but often turns into years of financial strain.

Even investments now are being funded through loans.

It often begins with what looks like a smart move — taking a personal loan to invest in stocks or mutual funds. The math feels convincing: equity returns should beat the cost of capital. We often tend to overestimate our stock picking skills set and underestimate risk.

Markets do not move in a straight line. At the same time, the interest never takes a pause. When volatility hits, the maths starts to crack. What felt like a rational bet begins to weigh heavily. Debt and long-term investing are rarely a good match.

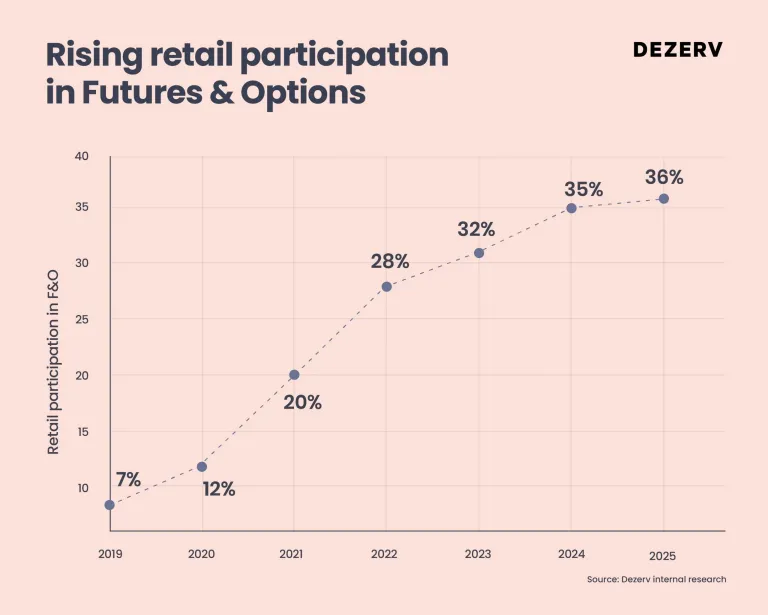

We’ve reached a point where people are taking loans to trade derivatives — using leverage to fund a product that is already leveraged.

Leverage Squared = Risk squared

It sounds extreme, but it’s more common than you’d think. Retail participation now makes up 36% of India’s total derivatives volume, a number that’s worrisome indeed. Many first-time traders treat option premiums as if that’s the only risk they’re carrying. They ignore the notional exposure, misunderstand mark-to-market losses, and mistake volatility for opportunity.

The bandwagon doesn’t stop here. My interactions with industry insiders reveal just how far this credit habit has seeped into mindsets. People are now borrowing to place bets on fantasy gaming platforms — using short-term loans or credit lines to fund what is essentially speculation.

This trend is alarming to say the least.

Here are some macro data points to confirm this broader trend and its deep entrenchment.

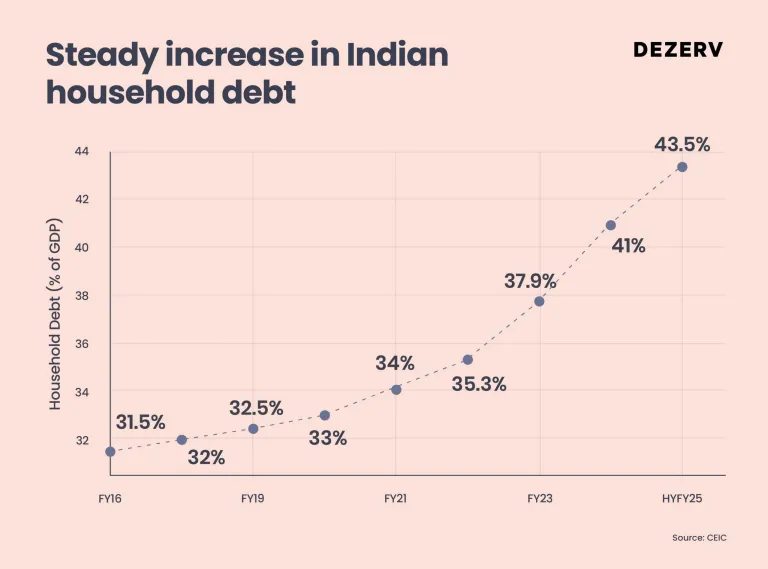

Household debt-to-GDP has risen to 43.5% in H1FY25, up from 31% a decade ago

This steady climb points to a structural shift in how Indians are financing their lives — with a growing share of consumption now funded through debt. While the absolute number may still trail developed markets, the speed of this rise signals a worrying reliance on leverage.

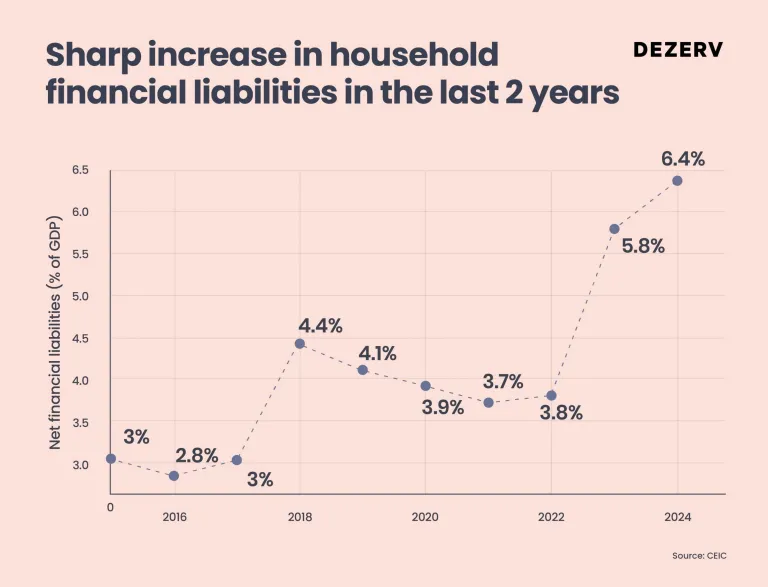

Net household financial liabilities rose to 6.4% of GDP in FY24

This is the highest in 17 years, just shy of the 6.6% peak seen in FY07.

Add to this the rise of built-in credit where EMIs are quietly offered at checkout on shopping apps, food delivery platforms, or even when you order groceries. You may not even realise you’re borrowing — until the bill arrives later. India’s financial system is no longer just enabling consumption. It’s being restructured around it.

Two pain points are rising to the surface —

1. Microfinance industry (MFI) pain-

The microfinance industry primarily caters to the underserved, lower-income households and informal borrowers, often in rural and semi-urban India. But this backbone of inclusion is now under visible strain. As of March 2025, gross NPAs in the microfinance sector have surged to 16%, up from 8.8% just a year earlier. CEOs across major banks and NBFCs have flagged this trend in recent earnings calls, highlighting rising delinquencies and repayment fatigue in the hinterland.

2. Rising credit card Non-Performing Assets (NPAs)

The signals are flashing red. Credit card outstanding balances have jumped from ₹1.1 lakh crore in December 2020 to ₹2.92 lakh crore in December 2024, a 165% rise.

What’s more concerning, though, is the pace of defaults. Gross NPAs now account for 2.3% of total outstanding, up from just 1% in 2020. The volume of unpaid dues has ballooned from ₹1,108 crore to ₹6,742 crore in four years — a sixfold increase.

The maths no one does – How small EMIs hide big traps

At some point, affordability stopped meaning “can I buy this?” and started meaning “can I service the EMI?”

Piling up of costs and interest: Take a ₹50,000 smartphone. On EMI, it feels light — ₹2,499 a month, no upfront payment. But stack up the processing fee, the inflated MRP, and the fine print on so-called “zero-cost” schemes, and you’re paying around 20-25% higher than the initial estimate. Often, the zero-interest tag only applies for the first three to six months. After that, interest quietly kicks in, sometimes at rates upwards of 24%.

Reduced risk capacity: EMI obligations reduce a young professional’s ability to take career risks—starting a business, pursuing higher education, or switching to higher-potential roles. The wealthy understand that early career flexibility often determines lifetime earnings.

Opportunity cost amplification: When a 25-year-old takes a ₹8 lakh car loan, they’re not just paying ₹8 lakh plus interest. They’re sacrificing the compounding of that money over 40 years. At 12% annual returns, that foregone investment could have grown to over ₹3.8 crore by retirement.

The danger isn’t the amount, it’s the habit. Small payments don’t feel like debt. But repeated over time, they quietly compound into a financial drag.

The wealth creator’s perspective

Here are a few ways I have seen smart wealth creators approach debt –

- No EMIs until the age of 30 unless for income-generating assets

- Any lifestyle EMI must be matched by equal investment contributions

- Major purchases require a 6-month “cooling off” period to reflect on the decision

Actionable frameworks for wealth creators

The smart debt test: 4 simple questions

Before taking any loan or EMI, ask yourself these four questions:

1. Will this make me money?

- Does the debt fund something that generates income or appreciates in value?

- Examples: Business loans, rental property, equipment for work

- Decision: Go ahead if returns beat interest costs

2. Does this preserve my cash for better opportunities?

- Am I borrowing cheaply to keep cash free for higher returns?

- Examples: Home loans at 8% when you can earn 12% elsewhere

- Decision: Proceed if you have a clear plan for the freed-up cash

3. Is this just for convenience?

- Am I borrowing for cash flow timing, not because I can’t afford it?

- Examples: Credit cards paid monthly, short-term financing

- Decision: Use rarely and pay back quickly

4. Am I borrowing to fund a lifestyle?

- Does this fund consumption have a future value?

- Examples: Wedding loans, vacation EMIs, luxury shopping

- Decision: Just don’t do it

While most of us see the logic in the above framework, the implementation is where it gets tough. That brings me to the next segment –

Why we fall for the debt trap – status, psychology, and poor money habits

It is easier than ever to buy things. But it is harder than ever to know whether you should.

In the previous edition, I wrote extensively about how my relationship with money evolved — from growing up in a household that valued savings to spending my early career learning how wealth is built. That journey shaped my approach to money, risk and lifestyle. But for many today, those reference points don’t exist. And that is where the cracks begin.

What used to be an exception i.e. borrowing to meet a genuine need, has now become routine. EMIs are not seen as debt. They are seen as access. Access to experiences, upgrades, and convenience — all without the discomfort of waiting.

So, the question beckons, why do we still fall for it?

- Peer pressure is rarely explicit, but it is omnipresent. When those around you are constantly upgrading their phones, cars and holidays, staying put starts to feel like falling behind.

- Aspirations are expanding faster than incomes. The distance between what you earn and what you desire has grown wider, and credit has moved in to bridge that gap. EMIs offer an easy way to keep pace. The entire process is frictionless by design.

- Financial literacy is still dangerously low. What’s more concerning is how early the cycle now begins. I see young folks, smart, sharp people just one or two years into their careers, tying themselves to long-term EMIs— car loans, home loans, consumer credit. Often, these decisions are taken without fully understanding repayment schedules, interest costs, or the implications of job loss or income disruption.

- Consumption is becoming the default starting point. Instead of directing early income toward income-generating assets, upskilling or building an emergency buffer, the first major financial decisions are centred on consumption. What starts as an upgrade quickly becomes a fixed liability, eating into flexibility, savings and future opportunities.

Add to that a culture built on instant gratification and FOMO, where not having the latest thing feels like being left behind, and you get a population that is spending less out of need and more out of reflex without building a solid financial foundation.

Why we fall for the debt trap – status, psychology, and poor money habits

Australia offers an interesting case study. Despite high per-capita incomes, household debt-to-income reached 186% by 2022. The problem? Credit access expanded faster than financial education.

The lessons:

- Geographic inequality: Credit stress concentrated in specific regions, similar to India’s Tier-2/3 emergence.

- First-home buyer traps: Government incentives to buy homes led to over-leverage among young buyers

- Credit card stacking: Multiple cards with low minimum payments created hidden debt loads.

Policy response that worked: Australia implemented “responsible lending” laws requiring lenders to verify genuine affordability, not just serviceability. Mortgage defaults dropped 40% within two years.

What global experience tells us about India’s debt problem

Debt stress can become systemic with any of these triggers –

- Interest rate normalisation forcing EMI resets

- Economic slowdown reduces income while debt payments remain fixed

- External shock (geopolitical, commodity price surge) is straining household budgets

Understanding these global patterns allows strategic positioning ahead of the cycle, whether through defensive portfolio allocation, opportunistic real estate timing, or business model adaptation.

Final thoughts

This newsletter is not a critique of EMIs. As a wealth manager, that would be so counterintuitive. A healthy credit ecosystem is essential for economic growth — it drives consumption, funds opportunity and expands access. Just like any powerful tool, its value depends on how effectively and thoughtfully it is used.

There lies a fine line between using credit as a means of progress and relying on it as a crutch for lifestyle, and more often than not, we fail to notice when we’ve crossed it.

That’s where Klarna finds itself today. What started as a convenience-led payments platform became a system that fuelled spending without pause. Klarna has close to 100 million active users globally. For Q1CY25, the company reported losses of $99 million. Credit defaults across the board are surging- 41% of BNPL users in the US admitted to paying late at least once in the past year. As the cracks widen, investor confidence is eroding fast: Klarna’s valuation has plunged from $45 billion at its peak to under $7 billion, a collapse that reflects just how fragile the foundations of this lending model have become.

India is still early in that journey. The question is whether we can course-correct before it becomes unsustainable.

Because the goal is not to avoid debt. The goal is to stay intentional. To borrow with awareness. And to remember that the ability to delay gratification has always been the most underrated form of wealth.

Join over 300,000 wealth creators who receive our weekly finance, business, and wealth creation insights. Subscribe to the Create Wealth newsletter here – https://bit.ly/dezerv_newsletter

Disclaimer – The information provided herein is intended solely for educational purposes and does constitute financial advice. In the preparation of this material Dezerv has used information developed in-house and publicly available information and other sources believed to be reliable. The data, graphs, charts, analysis included in this newsletter are as of the date of the document and subject to change from time to time without notice. All trademarks, logos, and brand names mentioned are the property of their respective owners and are used for identification purposes only. The use of these names, trademarks, and logos does not imply endorsement or recommendation.