“War is the continuation of politics by other means.” — Carl von Clausewitz

Throughout history, wars have done more than redraw borders and topple regimes – they’ve fundamentally reshaped economic landscapes. When nations clash, the ripple effects extend far beyond battlefields, touching everything from commodity prices to global supply chains.

Over the last two weeks, tensions between India and Pakistan brought us uncomfortably close to conflict. While the ceasefire has thankfully held, this brief window of uncertainty gave many Indians their first glimpse of war’s economic shadow. But in reality, we’ve only seen a fraction of what true military conflict does to economies.

In this edition of The Create Wealth Newsletter I wanted to explore a key question:

4. Investor takeaway: strategies for investing in uncertain times

Let’s dive in.

Wars as economic shockwaves

When conflict erupts, it delivers uncertainty in its purest form. This uncertainty follows predictable patterns across markets:

When conflict erupts, it delivers uncertainty in its purest form. This uncertainty follows predictable patterns across markets:

Safe havens surge: Gold and the US dollar typically rally as investors seek safety and liquidity

Energy markets spike: Oil prices often jump dramatically, especially when key producing regions or shipping routes are threatened

Equities react: Stock markets typically see volatility, with sharper declines in regions closest to the conflict

But these first-order effects are just the beginning. The more profound impacts emerge over time through inflation, supply chain disruptions, and shifts in global trade patterns.

Let’s look at recent conflicts to understand these dynamics:

Russia-Ukraine war: A case study in economic disruption

When the Russia-Ukraine conflict started in February 2022, the economic effects were immediate and far-reaching:

Energy shock: Brent crude shot from $78 to over $130/barrel in just weeks, as markets feared disruption from one of the world’s largest oil exporters

Food security crisis: Wheat prices soared nearly 60%, as Russia and Ukraine together account for nearly 30% of global exports

Metals squeeze: Nickel, aluminium, and palladium all saw extreme price volatility, disrupting manufacturing supply chains globally

Eurozone inflation: Price increases doubled, reaching 10.6% by October 2022, as energy and food costs filtered through the economy

The conflict reshaped energy flows and altered trade relationships.

Red Sea crisis 2024: Supply chains under pressure

More recently, the Houthi-led attacks in the Red Sea have choked a vital trade artery, showing how regional conflicts can disrupt global commerce:

Over 20% of global container traffic has been rerouted away from the Suez Canal

Shipping insurance premiums have doubled in high-risk zones

Transit times between Asia and Europe have increased by 10-14 days

Major retailers have reported inventory delays and increased logistics costs

This seemingly “contained” conflict has added inflationary pressure at a time when central banks were finally making progress against rising prices. It demonstrates how even geographically limited conflicts can have global economic consequences.

The Central Bank dilemma: Inflation vs. growth

Wars create a particularly challenging environment for central banks and economic policymakers. They often face a no-win scenario:

The wartime economic trap:

Conflicts drive inflation through supply disruptions and commodity price spikes

At the same time, they slow economic growth through reduced trade and business uncertainty

This creates a “policy trap” – raise rates to fight inflation and risk hurting growth further, or keep rates low and risk letting inflation spiral

History shows this dilemma clearly:

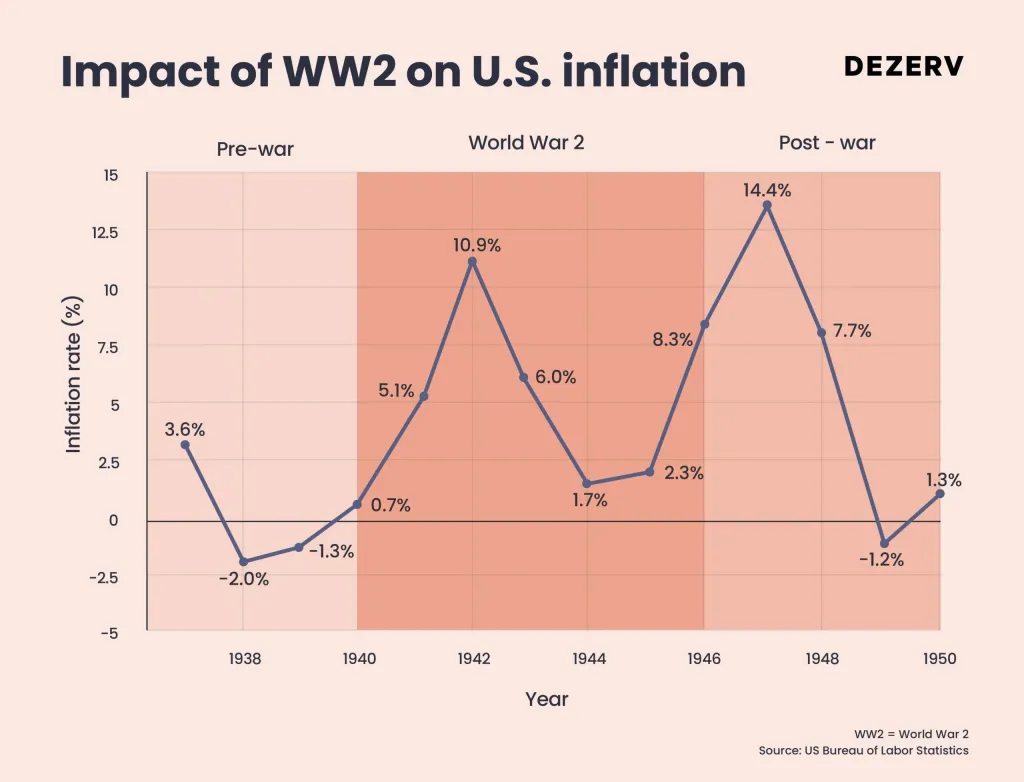

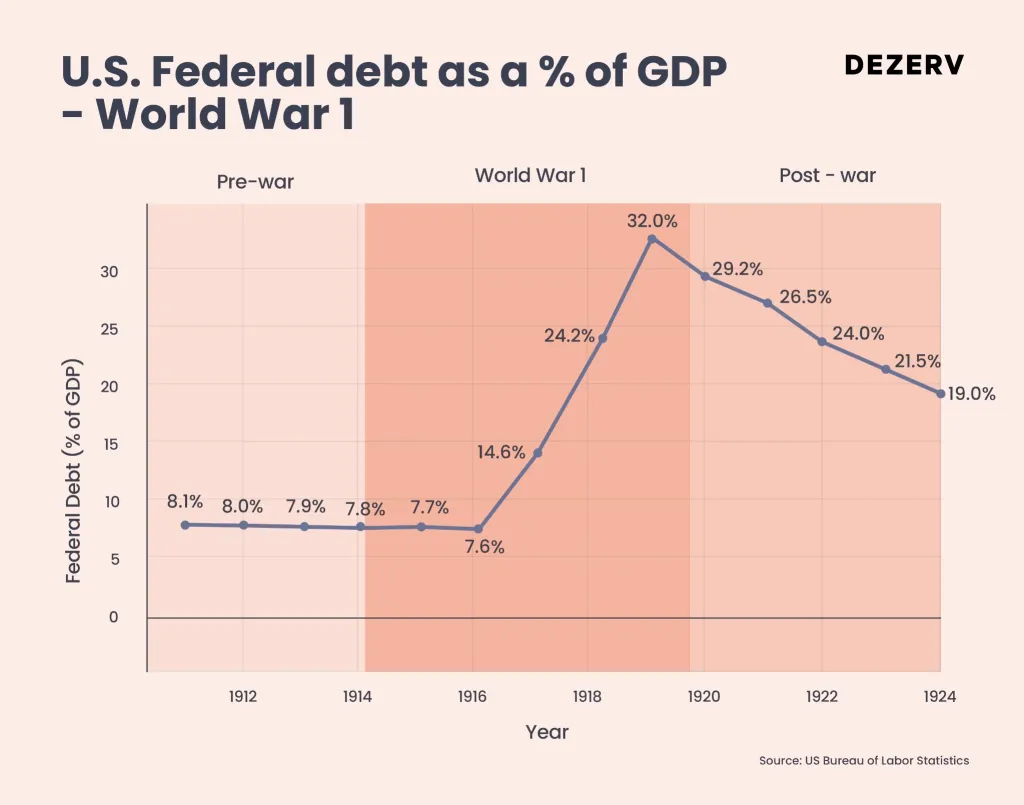

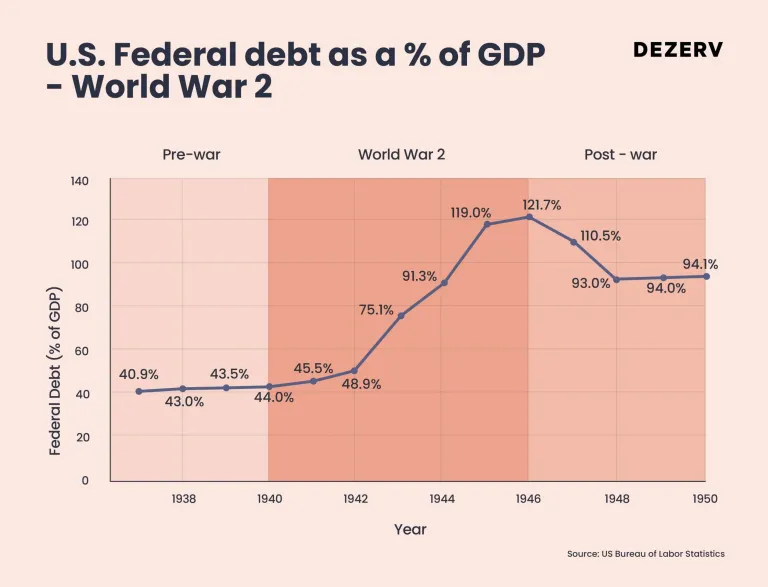

During World War I, U.S. inflation surged past 20% by 1918, while government debt nearly doubled as a percentage of GDP. World War II saw similar patterns, with inflation exceeding 11% and federal debt skyrocketing from 44% to over 119% of GDP.

In both cases, central banks kept interest rates artificially low to support war financing – creating what economists call “financial repression,” where inflation runs above interest rates and quietly erodes savings while reducing the real value of government debt.

To finance military efforts, the U.S. government expanded fiscal deficits dramatically, with federal debt rising from 16% of GDP in 1916 to over 33% by 1919, and again from 44% of GDP in 1940 to more than 119% by 1946.

A more recent example comes from the 1973 oil crisis, triggered by the OPEC embargo during the Yom Kippur War. Oil prices quadrupled in months, pushing U.S. inflation from 3.4% to 12.3%. The Federal Reserve’s delayed response – raising rates from 5.75% to over 11% – contributed to the painful “stagflation” era, where high inflation and high unemployment coexisted.

India’s experience during the 1990 Gulf War demonstrates how vulnerable oil-importing nations can be to conflict-driven energy shocks. When crude prices doubled, India faced a severe balance of payments crisis that ultimately forced:

The devaluation of the rupee by nearly 19%

The pledging of gold reserves as collateral for emergency IMF loans

Sweeping economic liberalisation reforms

This crisis, triggered by war-induced oil price shocks, ultimately reshaped India’s economic trajectory for decades to come.

The hidden costs of conflict

The true economic cost of war extends far beyond military spending. Even the brief escalation between India and Pakistan from May 7-10 illustrates this point.

According to the UAE-based Foreign Affairs Forum, India is estimated to have spent between ₹4,380 crore and ₹15,000 crore (approximately $519 million to $1.78 billion) during just this four-day period of heightened alert. This includes expenses for missile systems, drone operations, and military mobilisation.

Of course, due to security protocol, we don’t have details of the actual ammunition and machinery used, but the high-level equipment, which took years to procure and protected the lives of our civilians, definitely came at a steep cost.

But direct military costs represent only a fraction of the economic impact:

Broader economic costs:

Border economies suffer: Districts in Punjab, Jammu & Kashmir, and Rajasthan saw business disruptions, supply chain problems, and worker displacement

Transportation disruptions: Airspace restrictions force costly rerouting of commercial flights

Tourism impacts: Major cancellations affect hospitality businesses in vulnerable regions

Investment uncertainty: Capital flows slow as investors adopt “wait and see” approaches

The longer tensions persist, the deeper these effects become – even without a single shot being fired in actual combat.

Winners and losers in conflict economies

Wars redirect economic activity. This creates clear patterns of winners and losers across sectors:

Sectors that typically gain:

Defence and security: Military contractors, cybersecurity firms, and surveillance technology companies often see increased demand and government spending

Energy producers: Oil and gas companies typically benefit from supply disruptions and price spikes

Domestic manufacturing: Import disruptions often drive the reshoring of critical manufacturing

Alternative supply routes: Countries and companies offering trade bypasses around conflict zones can benefit

Sectors that typically suffer:

Aviation and tourism: These are often the first casualties of conflict, as we’ve seen with recent India-Pakistan tensions

Import-dependent industries: Manufacturers relying on global inputs face higher costs and uncertain supplies

Cross-border service providers: Banking, insurance, and consulting firms with multinational operations face compliance challenges

Consumer discretionary: As uncertainty rises, consumers typically delay major purchases

This reallocation of resources creates lasting structural changes in economies. After the Russia-Ukraine conflict began, for example, the iShares U.S. Defense ETF (ITA) has risen by approximately 60%, reflecting increased defence spending across NATO countries. In India, companies like HAL, BEL, and Bharat Dynamics have delivered strong returns driven by growing defence priorities.

Meanwhile, airlines like Air India face projected losses of over ₹5,000 crore if Pakistan airspace restrictions persist for a year, while IndiGo could lose around ₹1,300 crore, according to industry estimates.

Global supply chains: The invisible casualty

Perhaps the most profound economic impact of modern conflicts is their disruption of global supply chains. The intricate web of production and distribution that we’ve built over decades of globalisation is surprisingly fragile when geopolitical tensions flare.

How conflicts reshape supply chains:

From efficiency to resilience: The just-in-time model optimised for cost is giving way to “just-in-case” approaches that prioritise security

Friend-shoring replaces offshoring: Companies are relocating production to politically aligned countries rather than simply seeking the lowest costs

Strategic inventories return: After decades of minimising inventory as a cost-cutting measure, companies are rebuilding stockpiles of critical inputs

Diversification becomes essential: Dependency on single sources – whether for energy, rare minerals, or manufactured components – is now seen as a strategic vulnerability

Recent conflicts have accelerated the restructuring of supply chains. Companies are now:

Mapping their supply chains to identify hidden dependencies

Building redundancies into critical production systems

Accepting higher costs in exchange for greater security

Investing in technologies that enable more flexible production

This shift represents a fundamental reversal of decades-long trends toward hyper-efficiency and global integration. The economic implications are profound: higher costs, changing trade patterns, and new investment priorities that will shape growth for years to come.

India’s strategic position: The advantage of neutrality

India has always adopted a policy of strategic neutrality – refusing to take sides while securing its national interests. This approach has yielded significant economic benefits:

During the Russia-Ukraine war, India increased its imports of discounted Russian crude, emerging as one of the biggest beneficiaries of Western sanctions. The share of Russian oil in India’s import basket rose from less than 10% before the conflict to over 40% by mid-2023, making Russia India’s largest oil supplier.

This strategic neutrality allowed Indian refiners to:

Buy crude at discounted prices

Process it into refined products

Export high-margin products to other markets

Ease pressure on domestic fuel inflation

Similarly, during the Israel-Hamas conflict, India maintained defence partnerships with Israel while voicing concerns about civilian casualties, preserving both strategic relationships and moral positioning.

In a world increasingly divided into competing blocs, India’s ability to maintain economic relationships across geopolitical lines is becoming one of its strongest competitive advantages.

Historical perspective: Markets and military tension

India’s markets have weathered military tensions, terrorist attacks, and even full-scale war, and generally emerged stronger. While initial reactions can be sharp, history shows recoveries are typically sharper:

In fact, in less than a few days of the India-Pakistan de-escalation, the Indian markets surged again. On Thursday and Friday, the Nifty again touched 25,000 levels, and we have seen the markets gain 10% since March ‘25.

This resilience reflects India’s robust growth fundamentals, institutional stability, and increasing global economic integration.

Looking forward: Economic preparedness in an uncertain world

As geopolitical tensions rise globally, economic preparedness becomes essential. This doesn’t mean constant crisis management, but rather building systems that can withstand shocks without catastrophic disruption.

For nations, this means:

Diversifying energy sources and critical supply chains

Maintaining sufficient foreign exchange reserves

Developing domestic manufacturing capacity in strategic sectors

Building flexible policy frameworks that can adapt to changing conditions

For businesses, it means:

Mapping vulnerabilities across global operations

Developing contingency plans for supply disruptions

Creating financial buffers to weather periodic market volatility

Investing in technologies that enhance operational flexibility

For individual investors, it means:

Owning uncorrelated assets that can act as portfolio stabilisers

Maintaining allocation discipline through market turbulence

Understanding that short-term volatility is the price of long-term growth

Recognising that economic adaptability is ultimately a source of strength

In summary

War’s economic impact extends far beyond the immediate headlines about market drops or commodity price spikes. The most consequential effects are often structural shifts that unfold over years or decades:

The post-WWII Bretton Woods system shaped global finance for generations. The 1970s oil shocks ended the post-war economic boom and ushered in a new era of inflation. The post-9/11 security economy fundamentally altered patterns of government spending.

Today’s conflicts – whether in Ukraine, the Middle East, or the tensions between India and Pakistan – are similarly writing economic history in real time. The key to navigating this environment isn’t predicting the unpredictable, but building systems resilient enough to withstand whatever comes next.

Wars are economic events with consequences that reach far beyond the battlefield – reshaping industries, altering trade patterns, and creating new imperatives for businesses and governments alike.

In my opinion, those who stick to the basics and remain calm are the ones who leverage opportunities and create wealth in the long run.

Join over 300,000 wealth creators who receive our weekly finance, business, and wealth creation insights. Subscribe to the Create Wealth newsletter here – https://bit.ly/dezerv_newsletter

Disclaimer : Investments in securities are subject to market risks, read all securities related documents carefully before investing. The information, analysis, and views expressed herein are for educational and informational purposes only and do not constitute investment advice, a recommendation, or solicitation to buy or sell any securities or financial instruments. The content is based on publicly available data, internal analysis, and historical context believed to be reliable, but no representation or warranty, express or implied, is made as to its accuracy or completeness. The past performance is not indicative of the future performance. Readers are advised to consult their financial advisor before making any investment decisions based on this material.